Publication date: July 12, 2026

Category: Investing

Summary

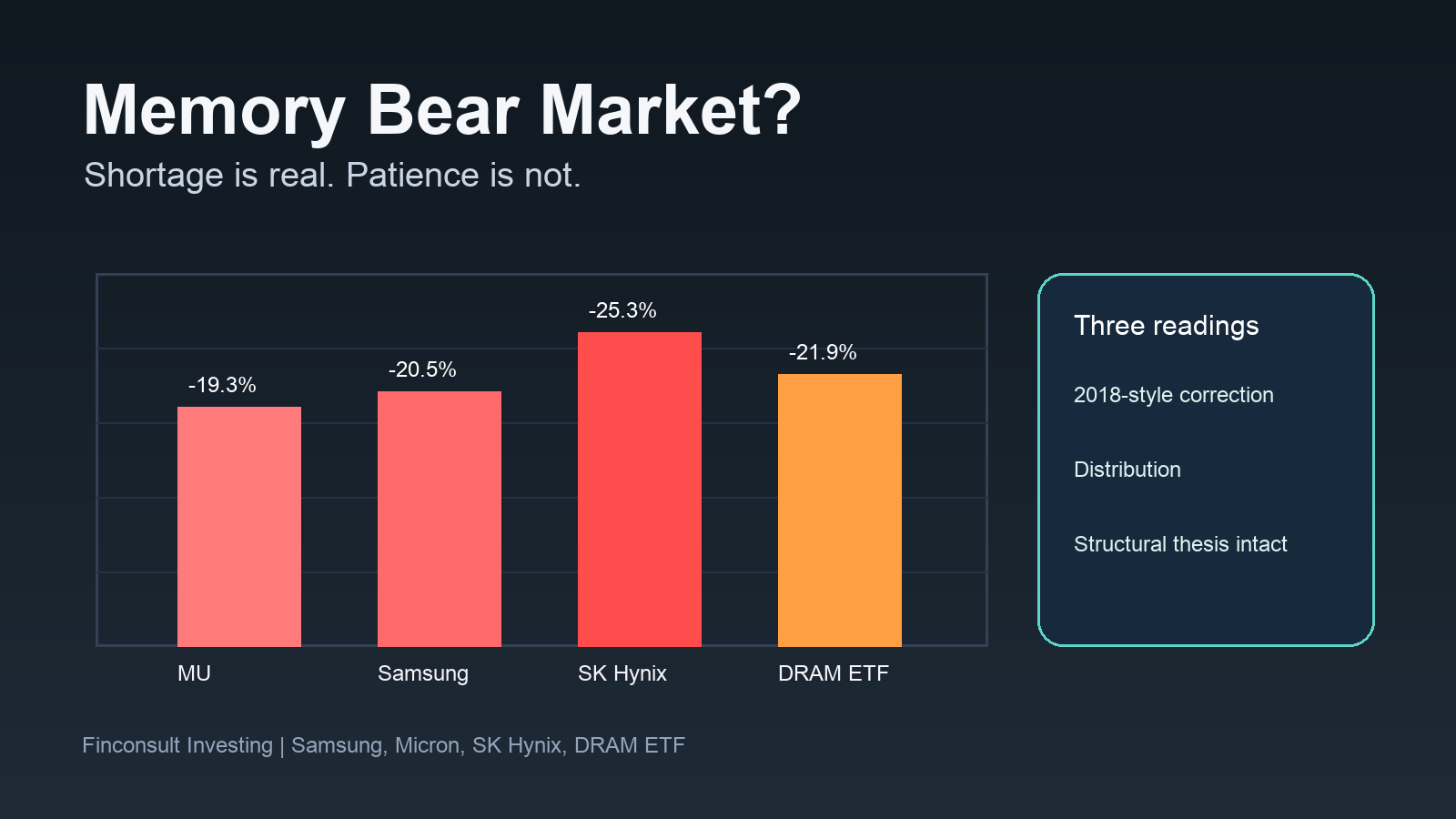

- Micron, Samsung Electronics, SK Hynix and the Roundhill Memory ETF have all fallen roughly 20% from recent highs, turning the memory bear market debate from a warning label into a live market test.

- The cleanest sentence for the current setup is this: the shortage is real, the market’s patience is not. A real HBM shortage can coexist with falling memory stocks.

- This is not yet a structural thesis collapse. It is a valuation, duration and positioning reset that could become either a 2018-style correction or the start of broader distribution.

(Advertisement)

Introduction: The Shortage Is Real. The Market’s Patience Is Not.

The phrase memory bear market sounds strange when the fundamental story still looks strong. AI servers need more high-bandwidth memory. Training clusters need more DRAM capacity. Inference systems still need faster memory access. Storage demand is being pulled higher by data-heavy applications, model checkpoints, synthetic data, video generation and enterprise AI workflows. If the world is building a larger AI machine, memory should be one of the cleanest beneficiaries.

Yet the stocks are no longer acting like clean beneficiaries. Yahoo Finance chart data show that Micron fell from a June 25 close of $1,213.56 to $979.30 on July 10, a drawdown of 19.3%. Samsung Electronics fell from KRW 358,500 on June 25 to KRW 285,000, down 20.5%. SK Hynix dropped from KRW 2,917,000 to KRW 2,180,000, down 25.3%. The Roundhill Memory ETF, ticker DRAM, declined 18.0% from its June 25 close and 21.9% from its June 22 six-month high. These are not random scratches on the paint. They are a sector-level repricing.

| Company / ETF | Ticker | Reference high | High price | July 10 close | Drawdown |

|---|---|---|---|---|---|

| Micron | MU | June 25, 2026 | $1,213.56 | $979.30 | -19.3% |

| Samsung Electronics | 005930.KS | June 25, 2026 | KRW 358,500 | KRW 285,000 | -20.5% |

| SK Hynix | 000660.KS | June 25, 2026 | KRW 2,917,000 | KRW 2,180,000 | -25.3% |

| Roundhill Memory ETF | DRAM | June 25, 2026 | $76.89 | $63.04 | -18.0% |

Yahoo Finance also framed the sector damage as roughly $1.5 trillion of semiconductor market value lost since June 25, while noting that Samsung’s record operating profit failed to impress investors. That is the sentence that should make memory bulls uncomfortable. If record profits do not move the stock, the market is not rejecting the past. It is questioning the future. Memory stocks do not fall only when earnings are bad. They often fall when earnings are excellent but investors begin to suspect that the excellent number is already owned, already extrapolated and already priced.

Why This Selloff Matters: The Samsung Contrarian Thesis Has Gone Sector-Wide

The most interesting part of the current selloff is that it has spread beyond one company. The contrarian Samsung thesis was never simply that Samsung’s earnings would disappoint. It was subtler than that. The argument was that Samsung could deliver strong numbers and still struggle if the market wanted more proof on HBM share gains, Nvidia qualification, NAND durability, foundry losses, capex discipline and shareholder returns. In other words, the stock could fall not because the business was weak, but because expectations had become too convenient.

That same logic now applies at sector scale. Micron is the easiest U.S.-listed pure play on the memory upcycle. SK Hynix is the execution champion in HBM. Samsung is the giant with catch-up optionality and balance-sheet firepower. The Roundhill Memory ETF packages the entire idea into a single trade. If all of them fall roughly 20% together, this is not a single-company controversy. It is the market auditing the memory thesis.

The audit has one central question: can a real shortage justify the price investors already paid? The answer is not automatically yes. A shortage can be real, and the stocks can still be ahead of themselves. HBM allocation can be tight, but a stock can still discount too many years of high margins. Server DRAM can be strong, but a forward multiple can still assume too much discipline from producers. AI capex can continue, but credit markets can still push back against long-duration infrastructure spending. The market does not pay for truth alone. It pays for truth, timing and surprise.

Is This a 2018-Style Mid-Cycle Correction?

Every memory investor eventually has to make peace with 2018. That cycle looked wonderful until it did not. DRAM profitability was strong, data-center demand was rising, and the industry structure seemed better than in the old commodity days. Then prices rolled over, inventory became a problem, estimates came down and stocks that looked cheap on peak earnings became cheaper. The painful lesson was simple: memory stocks often look most attractive on trailing numbers near the top of the cycle.

There are obvious reasons why 2026 is not a simple copy of 2018. HBM is qualitatively different from generic PC or smartphone DRAM. It requires more advanced packaging, deeper customer qualification, more complex capacity planning and closer ties to accelerator roadmaps. AI servers are not merely adding a little more memory content; they are reorganizing system economics around bandwidth. That makes the structural thesis more powerful than an ordinary commodity restocking story.

| Framework | What has to be true | Market behavior |

|---|---|---|

| 2018-style mid-cycle correction | Spot prices wobble, inventories normalize, but AI/server demand remains intact | Short, violent drawdown; leaders recover first |

| Classic memory distribution | Stocks fall before earnings roll over; estimates stay too high for too long | Lower highs, failed rallies, margin expectations reset |

| Structural thesis intact | HBM and AI memory remain bottlenecks; supply response is still disciplined | Correction becomes an entry window, not a cycle peak |

Still, the 2018 comparison should not be dismissed. The danger in memory is rarely that everyone suddenly forgets why memory matters. The danger is that supply, price and inventory move faster than the story. Investors can be right about long-term AI memory demand and wrong about the next twelve months of stock performance. A mid-cycle correction becomes healthy if earnings expectations remain supported and the leaders recover first. It becomes distribution if rallies fail, estimate cuts arrive late and the market begins selling good news.

Samsung: Why Record Profit Was Not Enough

Samsung is the cleanest example of the patience problem. A record operating profit should, in theory, be a victory lap. In memory, it can also be a warning. The market does not simply ask whether the number was big. It asks what created the number, whether the mix was high quality, whether HBM is gaining share, whether NAND is recovering sustainably and whether non-memory businesses are still absorbing capital. A record profit is useful only if investors believe it is not the last beautiful page before the chapter turns.

Samsung’s issue is not that it lacks scale. It has scale, manufacturing depth, cash, customer relationships and technology breadth. The issue is that investors have a more complicated scorecard for Samsung than for SK Hynix or Micron. They want evidence that HBM execution is improving, that the Nvidia-related qualification story is real, that NAND is not merely enjoying a temporary bounce, that foundry losses are narrowing and that shareholder returns can become more visible. A single profit headline cannot answer all of those questions.

This is why Samsung’s selloff should not be read as purely bearish. It is a test. If Samsung proves that HBM catch-up is accelerating, memory prices remain firm, capex stays disciplined and buybacks or dividends become more meaningful, then the selloff could become a delayed entry point. If profit strength is mostly a commodity-price spike while HBM share remains uncertain and capital intensity remains high, the selloff becomes a warning that the market has started to discount peak-cycle risk.

Micron and SK Hynix: Even the Best Stories Have Duration Risk

Micron and SK Hynix matter because they were not supposed to be the weak links. Micron is the U.S. market’s cleanest memory expression. SK Hynix is the company most associated with HBM execution leadership. When these two names drop sharply, investors should think less about company-specific disappointment and more about duration risk. A great thesis can still become a bad trade if the market has already capitalized too much of the future.

Micron’s valuation screen looks seductive. Yahoo Finance showed MU at a July 10 close of $979.30, an intraday market capitalization of about $1.106 trillion and a trailing P/E around 22. That does not sound outrageous for a company linked to AI infrastructure. But memory investors know that trailing P/E is a slippery tool. When the cycle is strong, trailing earnings look wonderful. When the cycle turns, those earnings become a postcard from a place investors can no longer visit. The real question is not whether Micron is cheap on last year’s numbers. It is whether 2027 and 2028 margins can justify the market cap after the AI memory premium.

SK Hynix has the opposite problem: the execution story is excellent, so expectations are extremely high. HBM leadership is a real asset. Customer trust is a real asset. But once a stock becomes the cleanest way to own an important bottleneck, the market begins pricing it as if the bottleneck will remain tight and monetizable for a long time. A 25% drawdown does not mean SK Hynix has lost its HBM crown. It may mean that investors finally noticed the crown was expensive to wear.

Roundhill Memory ETF DRAM: Pure Play Cuts Both Ways

The Roundhill Memory ETF is a useful sentiment gauge because it packages the structural thesis. Roundhill describes DRAM as the first memory stock ETF and says the fund seeks exposure to a precise basket of global memory chip companies. Its website frames memory as a secular growth story tied to the multi-decade buildout of AI infrastructure. Yahoo Finance lists major exposures including SK Hynix, Samsung Electronics, Micron, Sandisk and Seagate.

That is attractive because memory is no longer just a component line buried inside broader semiconductor funds. Investors can now buy a targeted memory basket. But pure exposure also means pure drawdown. If the market decides to sell the memory factor, DRAM does not get much help from a different semiconductor theme. Nvidia can have its own story. Broadcom can have its own ASIC story. TSMC can have its own foundry story. The memory ETF is there to answer one question: do investors still want the memory shortage trade?

The launch timing matters too. DRAM began trading on April 2, 2026, according to Roundhill. It arrived into a market already fascinated by HBM, AI data centers and memory scarcity. That does not mean the ETF marked the top. It does mean a lot of early buyers may have entered after the story had become easy to explain. In markets, the easiest story to explain is often the hardest one to buy well.

Investment Implications: Do a Thesis Audit Before Buying the Dip

The lazy bullish answer is to buy the dip. The lazy bearish answer is to declare the cycle over. A better answer is to perform a thesis audit. Investors should write down exactly what they own. Are they buying HBM shortage? Commodity DRAM recovery? NAND normalization? Samsung catch-up? Micron operating leverage? SK Hynix execution premium? Or simply the word AI attached to memory? These are different trades, and they deserve different risk controls.

| Signal | What to watch next | Interpretation |

|---|---|---|

| Bullish | HBM allocation remains tight, customer prepayments rise, capex stays disciplined | Shortage thesis survives |

| Neutral | NAND improves but commodity DRAM softens; analysts cut only outer-year margins | Range-bound digestion |

| Bearish | Lead times shorten, spot prices roll over, hyperscaler capex slows, inventories rebuild | Distribution risk rises |

The first signal to watch is lead time. If HBM allocation remains tight, customers commit to longer contracts and prepayments remain visible, the shortage thesis is alive. The second signal is spot pricing. Spot DRAM can wobble without destroying the cycle, but a persistent spot decline that later pulls down contract pricing would be more serious. The third signal is inventory. Memory bull markets usually die in inventory. Customers can say they are short while quietly building buffers. When buffers become visible, pricing power changes quickly.

The fourth signal is capex. The structural thesis requires supply discipline. If producers respond to high margins by adding too much capacity, the market will revive its 2018 playbook. The fifth signal is hyperscaler capex. AI infrastructure demand is not independent of financial conditions. If bond investors push back, if power bottlenecks delay data centers or if cloud customers become more disciplined about AI return on investment, memory estimates will have to adjust.

So Is This Distribution?

Distribution is not a single red candle. It is a process. It happens when strong hands gradually sell into good news, when rebounds get weaker, when analysts keep defending estimates while stocks refuse to respond, and when the market begins to treat record profits as yesterday’s story. Some elements of that pattern are visible now, especially the failure of good news to generate durable buying. But the full distribution case still needs more evidence: contract price weakness, inventory buildup, capex overreach, customer order cuts or a clear change in hyperscaler spending behavior.

That is why the correct conclusion is uncomfortable but useful. This is not yet a confirmed memory bear market in fundamentals. It is a confirmed bear market in patience. The market is no longer willing to pay any price for the shortage narrative. It wants proof that the shortage can survive price increases, customer budgeting, supply response and valuation gravity. That proof may arrive. If it does, the current drawdown could become one of the better entry points in the AI memory cycle. If it does not, the stocks may still look cheap all the way down.

Conclusion: The Shortage Can Be Real and the Trade Can Still Be Crowded

The memory thesis is not dead. HBM remains strategically important. AI servers remain memory hungry. Samsung, Micron and SK Hynix operate in a more concentrated and more technically demanding industry than the old commodity-memory stereotype suggests. Roundhill’s DRAM ETF exists because investors have a legitimate reason to want targeted exposure to memory and storage bottlenecks.

But the selloff is not meaningless. A 20% sector-level decline after strong earnings headlines tells us that the market has moved from belief to verification. Investors no longer want to hear that memory is scarce. They want to know how long it stays scarce, who captures the margin, whether customers over-ordered, whether producers stay disciplined and whether AI infrastructure spending can keep expanding without financial pushback.

The phrase to keep is simple: the shortage is real, the market’s patience is not. That is not a bearish slogan. It is a discipline slogan. Bulls can still be right, but they now need better evidence. Bears can still be early, but they now have price action on their side. The next phase will be decided by lead times, spot prices, inventory, capex and hyperscaler behavior. Until those signals clarify, memory is no longer just a structural thesis. It is a thesis on trial.

Related Topics

- SK hynix ADR Listing: Premium Analysis and Nasdaq-100 Potential

- Samsung PM1763 PCIe 6.0 Enterprise SSD and the AI Data Center Cycle

- Samsung Electronics Share Buyback and Capital Return Scenarios

Sources: Yahoo Finance chart API and quote pages for MU, 005930.KS, 000660.KS and DRAM; Yahoo Finance video headline on Samsung and the memory bear market; Roundhill Investments DRAM fund page; Finconsult calculations.

Language versions:

한국어 원문 |

English version